Top 4 reasons your residents want to report rent payments to credit bureaus

Credit reporting is a life-changing amenity for your residents and can also help you improve cash flow.

Why report rent payments to credit bureaus? Well, there are three kinds of residents. The residents you hope renew their lease, the residents you hope don’t renew their lease, and the residents you’re actively trying to evict. But all too often, the squeaky wheel gets the grease.

The “Karens” yelling at their phone provider’s poor customer service rep, demanding to speak to a manager, are the ones who get a free month of phone service. While the customers who pay their bills on time and never call to complain – get nothing.

Are you giving your best tenants enough credit? You want your favorite tenants to stay. However, you devote more energy to the ‘squeaky wheels.’ Letting your residents report rent payments to credit bureaus requires no effort on your part, but is a game-changer for your best tenants.

Here are 4 reasons why your residents want to report rent payments to credit bureaus:

- It’s the easiest way to build credit for a large expense without debt

- They can finally take advantage of positive reporting

- Everyone can benefit from it, no matter their score

- Improved credit helps residents achieve their goals

FREE DOWNLOAD Download 5 proven steps to reach 100% digital rent payment adoption to learn how rental credit reporting is a great incentive for online payments.

Want to boost digital payment adoption?

1. Reporting rent payments to the credit bureaus is the easiest way to improve a credit score

It’s convenient

Typically, adults in their early thirties are making those quintessential “big life decisions.” They’re getting married, starting a family, or buying a house. For the lofty purchases that involve a lender, they’ll need a good credit score.

Over 60% of Americans under the age of 35 are still renting. So the majority of young adults gearing up to make those big life purchases will be on the lookout for opportunities to add to their score. There might never be a more convenient way to hit this goal than rent payment reporting. The process is shockingly simple: opt-in, pay rent as usual, and watch their credit score improve.

It’s fast

Best-in-class rent reporting services will report rent payments to credit bureaus the day after the payment has been verified. Then it usually takes about two weeks for the credit bureaus to update the resident’s credit report.

People will work on their credit score for years, applying for credit cards and opening new tradelines, only to see a minor uptick. However, studies show residents who opt-in to report rent payments to credit bureaus, see their credit scores increase by an average of 29 points after just two months.

2. Residents can finally take advantage of positive reporting

Why should we reserve positive reinforcement for puppies and toddlers? Adults want to be rewarded for smart choices and good behavior too. Maybe not with dog treats or an ice cream cone, but with financial incentives and lifestyle enhancements.

Where is the positive reinforcement for paying rent on-time, every time? In most cases, there is no reward. But there is a looming threat – a single late payment can damage their credit score. And that’s frustrating for residents who diligently track their finances to ensure rent is paid on time. With rent payment reporting, punishment is no longer the only option. They’ll finally have the opportunity to reap rewards for their good behavior.

The bad news for your residents

Unlike an auto loan or a mortgage, property management companies do not automatically report rent payments to credit bureaus. Along the same lines, gas & electric companies do not automatically report positive utility payments to the credit bureaus. However, if a resident forgets to pay their electric bill one time, their score drops and their credit history suffers.

Specifically, if a payment is considered late for over 30 days, the resident’s credit score will immediately drop by about 10 points. And it will continue to drop with every month that the utility bill is left unpaid. To make matters worse, that late payment will remain visible on their credit report for 7 years.

Moral of the story is, life’s not fair. People don’t automatically get the good credit they deserve for years and years of positive, on-time utility payments. But if just once, they forget to (or can’t afford) a payment, their credit suffers. However, there’s hope.

The good news for you both

Delinquent payments are no longer the only rent-related payments that can affect a resident’s credit score. With a best-in-class payments platform, you can offer your residents the chance to reap the rewards of their good efforts.

Responsible residents set up AutoPays to make sure their rent, utilities, ancillary fees, etc. are paid to you in-full, and on-time. If a steady cash flow is important to your business, helping your reliable renters build credit is a small token of appreciation you can easily offer.

Credit should be a two-way street; negative strikes for delinquent rent payments, and improved credit for positive payments.

3. Everyone can benefit from reporting rent to build credit, no matter their score

Be the hero – help those who need it most

Rent payment reporting is a powerful tool that can benefit anyone – no matter their age, income level, or current score. However, this amenity is especially compelling when it comes to the “credit invisible.”

What classifies someone as “credit invisible”?

“Credit invisible” is a term used to define consumers who have zero credit history with any of the three nationwide credit reporting agencies (Equifax, Experian, and TransUnion). Currently 26 million Americans are classified as “credit invisible.”

Mortgage lender, Travis Bourassa, has worked with many young and eager home buyers who thought they were ahead of the game. In reality, they hadn’t even started playing. They’d boast about their lack of debt because they’ve never owned a credit card. Their hand-me-down car meant they never missed an auto payment, because they don’t have an auto loan. And they’re saving money by staying on their parents’ family phone plan.

All of that is fantastic, and fiscally responsible. But it means these hopeful homebuyers don’t have any lines of credit being reported. So if Travis were to check their credit report, they’d have a 0 credit score – making them “credit invisible.”

So what is Travis’s advice to the “credit invisible”? Get a secured credit card, and make absolutely sure it reports to all three major bureaus. This is the first step to building credit. Then take advantage of services that will report rent payments to credit bureaus, which don’t require a hard inquiry (or “hit”) on your credit report.

Rent reporting for subprime consumers

Unlike the “credit invisible,” subprime consumers have a credit score, but it’s not one that potential lenders, employers, or landlords will be impressed by. Experian defines subprime borrowers as those with a FICO® score below 669. And approximately 19% of the U.S. adult population has either subprime or deep subprime credit. Which means:

Paying off debt little by little can take several months or even years to make any significant impact on a subprime credit score. One very effective solution is hiding in plain sight.

Paying off debt little by little can take several months or even years to make any significant impact on a subprime credit score. One very effective solution is hiding in plain sight.

Reporting rent payments to credit bureaus for everyone else

Residents with credit scores classified as “good” or even “great” might think – I’ve already got a decent credit score, I don’t need rental payment credit reporting. But that is a proven misconception. No matter age, credit score, or income level, the opportunity to report rent payments to credit bureaus benefits everybody.

Pinnacle manages mostly Class A & B properties. Unsure if rental payment credit reporting would be beneficial for their tenants, a member of the Pinnacle leadership team decided to put it to the test.

At the time, his daughter was in her thirties, living in a Class A property in New York City, making six figures, and boasted a 728 credit score. So her Dad enrolled her in rent payment reporting program to see what would happen.

They revisited her dashboard after 3 months. Her score had already moved from 728 to 750. In the credit world, even bumping your score by 22 points can make a significant difference in the types of rates lenders will offer you. Case in point – everyone can benefit. Pinnacle signed up.

4. Rent reporting helps residents achieve their financial goals

Report rent to credit bureaus & empower your residents

Obviously credit scores and credit history are huge determining factors in the level of financial help your residents are eligible for. Credit affects what down payments and interest rates will be available to them for everything from auto loans, to cellular plans, to mortgages.

You want to avoid turnover. You especially want to retain the residents who pay on time. And while a significant % of the millennial generation have been slower to purchase a home, ideally most don’t want to rent forever.

It’s true. Millennials are attracted to the luxurious style of living found in an amenity-rich apartment community. An urban oasis situated only blocks from their office or favorite local coffee spot. But buying a house is still the American dream. In fact, 40% of millennials are actively saving to purchase a home, and 31% of millennials said they expect to own property in the future, but aren’t currently saving for a down payment. Take advantage of being able to appeal to that 71% of millennial renters who are hoping to purchase a home someday.

Also, make your management company sticky. If a resident was debating a move, the fact that your company will report rent payments to credit bureaus might sway them to renew their lease with you instead. Especially once they see how rental payment reporting has added to their credit. Remember, if you offer this program, you’re in the 17% of property management companies that do.

How credit bureau scores influence home buying

In the mortgage world, credit is huge. It’s the most integral factor when it comes to lending. Of course, there are a lot of considerations when it comes to mortgages, but the foundational factors lenders look at are income and credit.

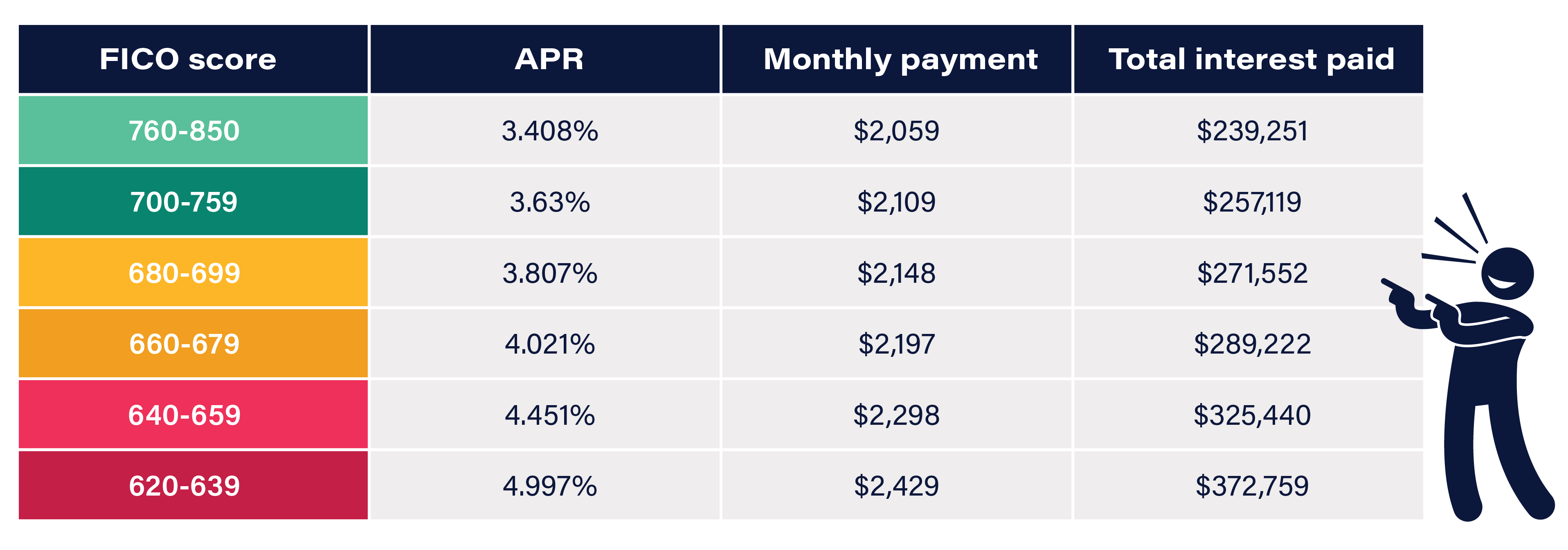

Mortgage lenders look at credit scores in tiers. Using mortgagecalculator.org in June of 2020, we are able to provide a broad representation of how one’s credit score can directly impact dollars spent or saved. Keep in mind that APRs change constantly, so these numbers may no longer be perfectly accurate. The purpose of this chart is to help paint a general picture.

This table assumes a home value of $500,000, with 20% down, and a 30 year loan term.

Looking at that table, the difference in total interest paid over the length of the loan can add up to over one hundred thousand dollars depending on credit score. Using a tool to report rent payments to credit bureaus could potentially save someone tens or even thousands of dollars down the road. That’s one heck of an ROI. Everyone should be making that investment.

Looking at that table, the difference in total interest paid over the length of the loan can add up to over one hundred thousand dollars depending on credit score. Using a tool to report rent payments to credit bureaus could potentially save someone tens or even thousands of dollars down the road. That’s one heck of an ROI. Everyone should be making that investment.

But that’s not the only mortgage-related benefit. Rent payment reporting also speeds up the lending process. If they’ve been using a program to report rent payments to credit bureaus, the mortgage lender will be able to see their rental payment history directly on their credit report.

This saves them the trouble of having to call your property management company to track down the resident’s payment information. And it’s one less administrative task you and your team don’t have to handle anymore. Less admin work is always a plus.

Additional ways to leverage improved credit from reporting rent payments to credit bureaus

As we’ve established, building good credit opens the door to lower interest rates on credit cards, home loans, car loans, and more. They’ll get better rates when they:

- Want the best reward credit cards

- Upgrade their apartment

- Switch or apply for car insurance

- Take out student loans

- Take out personal loans

- Lease/buy a car, boat, motorcycle, etc.

- And more

With countless benefits, your residents have no reason not to enroll in a rent payment reporting program. And you’ll be able to help drive digital payment adoption across your portfolio.

Start reporting your residents rent payments

With Zego Pay credit reporting, offer residents a unique benefit when they pay rent online. Providing rent payment credit reporting can also help you attract and retain more responsible residents. Book a demo with Zego today.